Information Related to "Don't Leave Home Without It"

| Audio/Video |

![]() Most

of us have seen or heard a commercial using the slogan, "Don't

Leave Home Without It." In one scenario, a woman is calling up a cab

company to tell them that all her vacation money is in the cab in which

she was riding. She is now without any money in a large city and she's

far from home. The bottom line in this commercial is that if she had

been wise with her money, she would have carried the advertiser's product,

which would have insured her loss.

Most

of us have seen or heard a commercial using the slogan, "Don't

Leave Home Without It." In one scenario, a woman is calling up a cab

company to tell them that all her vacation money is in the cab in which

she was riding. She is now without any money in a large city and she's

far from home. The bottom line in this commercial is that if she had

been wise with her money, she would have carried the advertiser's product,

which would have insured her loss.

Money is a tool and everyone needs the knowledge and understanding to properly

use it. We can use it to make purchases using cash, checks, credit and

debit cards. As a tool, we have the choice of spending our money or saving

it. We can use money wisely or foolishly. How well do you use the money

that is available to you? What knowledge concerning money do you need to

know before leaving home?

Money is a tool and everyone needs the knowledge and understanding to properly

use it. We can use it to make purchases using cash, checks, credit and

debit cards. As a tool, we have the choice of spending our money or saving

it. We can use money wisely or foolishly. How well do you use the money

that is available to you? What knowledge concerning money do you need to

know before leaving home?

Consider this person's story from the book, It Doesn't Grow on Trees, by Joan Ross Peterson: "Larry's parents gave him every advantage while he was growing up. He attended an excellent private school, went to camp in the summer, enrolled in a prestigious university, graduated, was married, and went to work in his father's company. Six years later, his father died and the company was bought by a competitor. As a result, Larry inherited close to a million dollars. 'It didn't take me long to lose it,' he told me, 'and now, even with my wife working, I'm worried about how I'm going to put my kids through college.' Larry's story is repeated over and over again by others; the only variant is the amount of money involved" (p. 12).

If you were to receive a sum of money, would you know how to use it wisely? How well are you, as a teen, able to manage your money? You may be saying, "I don't have much money so it doesn't matter how I use it." However, the way you manage the little money you have now will have an impact on the way you approach economic issues later in life. Let's consider some points concerning the basics of wise money management.

The first and foremost consideration about money and Christianity is that God must be in the picture. In the book of Proverbs, which is directed to the instruction of young people, the writer states: "In all your ways acknowledge Him [God], and He shall direct your paths" (Proverbs 3:6). As you follow God's instructions regarding finances, you can avoid many pitfalls that cause people great sorrows (1 Timothy 6:9-10).

We learn more about how we can honor God in all our ways in Proverbs 3:9-10. "Honor the Lord with your possessions, and with the firstfruits of all your increase; so your barns will be filled with plenty . . ." In essence, the wealth that God gives to us is to be used to honor God.

One of the chief ways we can honor God with our possessions is by tithing. Tithing refers to giving a tenth of what we earn to God (Leviticus 27:32). In the book of Malachi, God says that failing to pay one's tithes is stealing from the Creator. However, God challenges individuals to tithe by saying, "' . . . And try Me now in this,' says the Lord of hosts, 'If I will not open for you the windows of heaven and pour out for you such blessing that there will not be room enough to receive it'" (Malachi 3:10). God promises blessings to the person who will acknowledge Him by returning a tenth of the profits for God's work.

How do you apply this as a teen? Do you do odd jobs around your neighborhood such as raking leaves or mowing lawns? Maybe you do baby-sitting for a neighbor or work at a fast-food restaurant. If so, when you are paid, make it a habit to return 10 percent to your Creator who has blessed you with the opportunity to earn some money. If we make tithing a habit, God promises to bless us.

After you've paid tithes, what should you do with the remainder? Advertisers bombard teens with a bountiful array of items on which to spend their money. The temptation is to spend what you earn immediately. But have you considered the impact of saving even a small portion of your earnings?

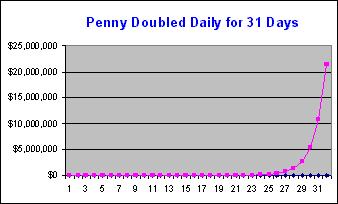

Taking a penny and doubling it each day for a month gives a vivid illustration

of what happens when you save a portion of your funds and invest them.

If you look at what has accumulated in seven days, you only have $1.28.

At this point it doesn't seem worth making the investment. However at the

end of two weeks you would have $163.84. That sum would not be a bad return

for a two-week period.

Taking a penny and doubling it each day for a month gives a vivid illustration

of what happens when you save a portion of your funds and invest them.

If you look at what has accumulated in seven days, you only have $1.28.

At this point it doesn't seem worth making the investment. However at the

end of two weeks you would have $163.84. That sum would not be a bad return

for a two-week period.

If you continue the process for a third week, you would have amassed $20,971.52. If you continued to the end of a 31 day month you end up with $21,474,836.48. This is a vivid illustration of what is called the miracle of compound interest. While real investments don't grow that quickly, even young people can take advantage of investing opportunities.

Speak to your parents, go the library and read about investing, speak to someone at your local bank or even search the Internet for information concerning getting started with a savings plan. As you start saving, your nest egg will not seem like much right away. But what you have to remember is that you are investing for the future. As you save a portion of the money you earn, it will grow into a valuable asset.

Many workers receive a paycheck, cash it, put it in their wallet and pay for the things they need as they go about their daily routines. It's not long until most of the money is gone or almost gone. Spending one's paycheck in this way results in a weekly or biweekly bind because when the money runs low, you have to worry about making ends meet.

As you earn your money, you can learn to avoid this frustrating situation by budgeting your money. A budget allocates funds for tithes, savings and then sets aside money for items you want or need. For instance, your parents may require you to pay for the insurance in order to drive a car. If you receive income and set aside a portion each time you are paid, when the bill for insurance comes, you will have the money. Also, if you want to buy a particular item, you can set aside money on a regular basis so you can eventually make the purchase.

Budgeting is merely choosing how you are going to allocate your money. Analyze what your spending priorities are and force yourself to stick to the goals you set. Realize also that there's nothing wrong with having some money that you can spend for fun. Just be sure to put it in as part of your budget.

In learning to handle your money, it would be helpful for you to open a checking account so that you can learn to keep track of money in such an account. If you open an account, try to find one that has the fewest fees possible. You may have to pay for checks, but you can usually find an account without additional charges. If you have enough money, you may be able to open a checking account that earns a little bit of interest.

Once you open a checking account, you must then keep track of it by entering deposits you make, checks you write and interest earned or fees paid. Keeping track of your checkbook can be done on a monthly basis by balancing your checkbook to the penny compared to the statement from your bank. Have a parent or a friend help you learn to do this.

By maintaining a balanced checkbook, you will know what's in your account and be able to avoid writing checks that don't have money to back them. Writing a check you don't have enough money in your account to pay is called an overdraft. Overdrafts usually end up costing you $20 or more per overdraft, depending on the bank policy. Keeping track of your checking account helps you make the most of your money and avoid paying unnecessary fees.

Many checking accounts offer ATM cards that allow you to do your banking

and get cash at a machine outside of business hours. Ask if there are any

fees involved. Be aware of any fees before you decide to get one of these

cards.

Many checking accounts offer ATM cards that allow you to do your banking

and get cash at a machine outside of business hours. Ask if there are any

fees involved. Be aware of any fees before you decide to get one of these

cards.

Finally, debit cards are offered with some checking accounts. A debit card is not a credit card. It is a card that is swiped like a credit card, but the amount of the purchase is immediately deducted from your checking account. If you use a debit card, it is essential that you know the balance in your checking account to avoid overdraft charges.

The Bible tells us, "Be diligent to know the state of your flocks, and attend to your herds" (Proverbs 27:23). This means we should carefully watch over those things that are our responsibility. Knowing the state of our finances is one area that must be diligently watched to avoid potential pitfalls.

Once you graduate from high school, you will begin to receive a never-ending array of phone calls and promotional offers encouraging you to apply for a credit card. As you receive these offers, you must ask yourself if you are ready to take on the responsibilities.

Are you ready to pay the fees that are involved? Each year you may have an annual fee. If you use the card for a cash advance, there is a fee involved and if you don't pay the cash advance back by the next billing cycle, you will have to pay interest.

Finally, if you make purchases and cannot pay for them by the due date, then the company will begin charging you interest. Remember that many credit cards are easy to get, but they are hard to pay for when they are charging you between 18 and 21 percent per year on the unpaid balance. They will offer you the opportunity to pay a minimum balance, but realize there is a hefty interest charge that continues until the entire balance is paid off.

The best way to use credit cards is to pay no fees and have the credit card company give you a rebate at the end of the year. You can achieve this goal by avoiding the purchase of any item that you cannot pay for when the bill arrives. In this way you can have the convenience of a credit card, but you are using it to your advantage.

Part of your preparation for life is to know how to use money wisely. Wisdom with money begins with honoring God with your possessions. This overriding principle is followed by learning to discipline yourself to save a portion of the funds you earn, by keeping track of the money you spend and by being careful to avoid the financial pitfalls previously covered.

As the commercial advises each of us to avoid leaving home without their product, you might consider these points about money management and resolve to not leave home without understanding them.

If you'd like to learn more about money management, request the free booklet, Managing Your Finances. It is available for viewing, downloading or ordering. YU

About the author:Related Information:

Table of Contents that includes "Don't Leave Home Without It"

Other Articles by Gary Smith

Origin of article "Don't Leave Home Without It"

Keywords: teen budgeting teen tithing teen saving teen credit

Tithing: